Income Share Agreements: A Win For Investors And Students?

Income Share Agreements: A Win For Investors And Students?

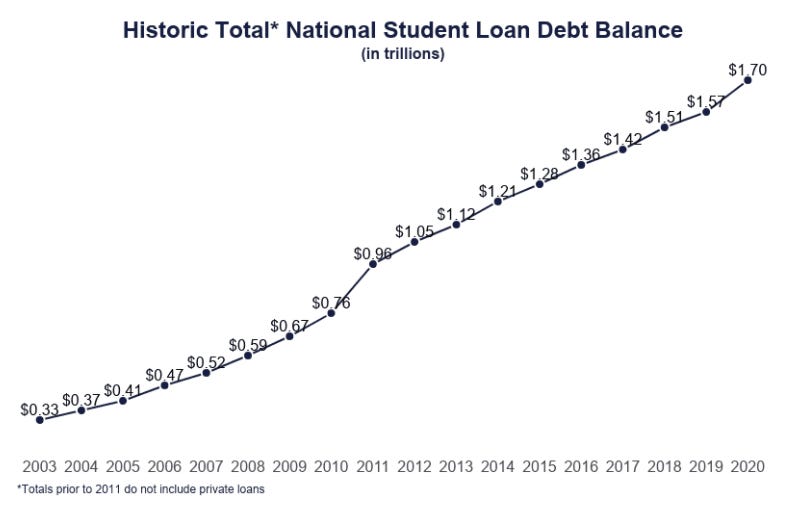

Leaving college with thousands of dollars in student loan debt is a stark reality for many young Americans. In fact, America currently owes a massive $1.73 trillion in student debt.1 The lucky ones rely on family to pay their way, but many more rack up huge debts which have to be repaid regardless of their income after graduation. That’s where an Income Share Agreement or ISA comes in. Instead of taking out a loan at a fairly high interest rate, an ISA provides capital to pay college fees in return for a share of the student’s future earnings over a specified term.

Income Share Agreements might sound like a pretty sweet deal both for students and investors. So, what’s the catch? Let’s walk through how these agreements work and see if it’s really as good as it seems.

How Do Income Share Agreements Work?

An ISA is a form of human capital investment, an idea first proposed by Nobel laureate economist Milton Friedman in 1955. The basic principle is that human capital should be treated as an asset consisting of the expertise, experience and skills of individuals.

Friedman proposed human capital contracts whereby an individual could be provided with some initial capital to enhance their skills or expertise through training or education. In exchange the investor would receive a share of their income over a specified time period.

Most modern ISAs work by providing upfront funding for a student’s education. The student will then repay a fixed percentage of their future income on a monthly basis. This repayment usually only begins once the student passes a certain minimum income threshold, with repayments made over a fixed term up to a maximum cap amount.

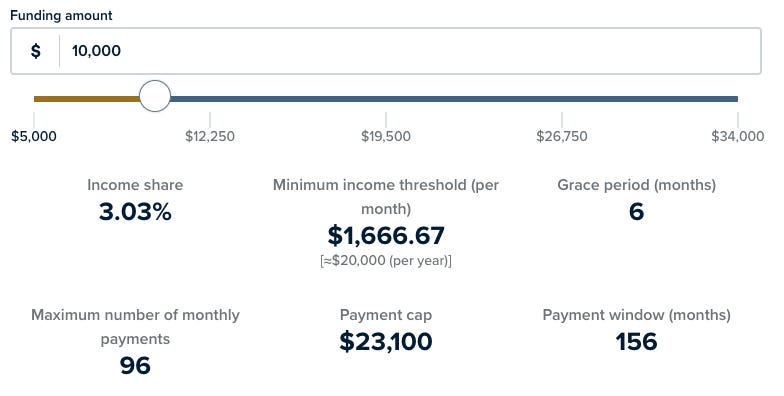

The example below is taken from Purdue University’s ISA Comparison Tool and shows the repayment terms for a student studying Civil Engineering who needs to borrow $10,000.

For investors, ISAs can be an interesting option to receive passive monthly income and diversify your portfolio by investing in the next generation. Most providers carefully screen students, only selecting top achievers studying at leading schools who are most likely to deliver strong and stable yields.

Preferred majors include Computer Science, which boasts a starting salary of $132,500 for Columbia University graduates, and Business, Economics & Finance, with a starting salary of $160,600 for Berkeley graduates.2

Income Share Agreements Vs Traditional Loans

Key Players

Since Milton Friedman revealed his big idea in the 1950s, various colleges and private lenders have experimented with ISA offerings. Examples include Purdue University, which offers an ISA as a supplement to a traditional student loan, the University of Utah, and Make School, a startup school offering bachelor’s degrees in applied computer science. The University of San Diego Extension also offers an ISA for students looking to get certified as a digital developer, software developer, digital marketer or business analyst.

More relevant to investors are the third-party ISA providers which work with schools to offer alternative funding options. Examples include Mentorworks and Blair which raised $100 million from a large institutional capital partner at the start of 2021 to fund ISAs at partner institutions.

There are also some private providers which offer ISAs directly to students rather than through a particular school. Align provides an ISA of up to $12,500 with 2-4 year payment terms and is funded by institutional investors. Edly refers to their offering as an “Income-Based Repayment Loan” rather than an ISA. Investment with Edly is restricted to accredited investors who either have net worth of over $1 million or income of at least $200,000 for the past two years. The minimum investment threshold for Edly is currently $10,000.

Pros & Cons For Investors

Now we’ve explored exactly how ISAs work and how investors can get involved, let’s dig into the pros and cons of this unconventional investment vehicle.

Pros

Passive monthly income: Providers typically pass on student repayments on a monthly basis. These usually begin small and increase over time as the earning power of the student grows.

Attractive returns: The “EdlyOutcomes I High Yield” account focuses on what they consider to be the most profitable students and programs and has a target return of 14%. Edly reports a historical return to their investors of 16.57%.

Diversification: ISA providers typically apply investor funds across income-based products from different schools and in different geographical locations and industry sectors.

Legally-Binding Contracts: The ISA provider signs a legally-binding contract with the student setting out the repayment terms.

Short maturation: Investors can expect full repayment within a relatively short term. According to Edly, this is typically 3-5 years.

Social Impact: ISA investments can come with philanthropic benefits for investors who are interested in causes like broadening access to education.

Cons

Risk: Students may drop out of their course or fail to secure a job over the minimum salary threshold required for repayment. To limit these risks, most ISA providers carefully screen schools, programs, and students to select those most likely to succeed and conduct thorough underwriting processes.

Regulation: ISAs are not regulated in the same way as private student loans. Regulators have been keeping a close eye on ISA providers in recent years. In September 2021 the Consumer Financial Protection Bureau took action against ISA provider Better Future Forward Inc., for falsely representing its product by claiming it wasn’t a loan and failing to comply with federal consumer financial law.3 Whether tighter regulation is on the horizon for ISAs remains to be seen.

Limited liquidity: Since there is currently no secondary market for ISA-type investments, investors should expect to be locked in for the full investment term.

Management fees: Investors may have to pay both a management fee and a percentage of cashflows. In the case of Edly, investors pay a management fee of 1% of the initial investment amount per year for 2 years plus 4% of cashflows.

Final Thoughts

For the moment, Income Share Agreements are restricted to wealthy accredited investors and the big institutional players. And even if you do have deep enough pockets to qualify, the recent move by the Consumer Financial Protection Bureau against a rogue ISA provider indicates tighter regulation may be on the cards.

On the flip side, the sheer volume of student debt suggests there’s plenty of room for alternatives to the traditional student loan. ISAs may be an imperfect solution, but they also give investors a small slice of America’s $1.73 trillion in student debt.

Disclosure:

This document is for informational purposes only and is not an offer or solicitation to purchase or sell securities. Investing involves risks, including the potential for principal loss. There is no guarantee that the strategies and services will be successful or outperform other strategies and services. Certain assumptions may have been made in connection with the analysis presented herein, and changes to the assumptions may have a material impact on the analysis or results.

Past performance is no guarantee of future results. The investments discussed herein may be unsuitable for investors depending on their specific investment objectives and financial position. Investors should independently evaluate each investment discussed in the context of their own objectives, risk profile and circumstances.

All opinions expressed herein constitute judgement as of the date of this article and are subject to change without notice. Statements made are not facts, including statements regarding trends, market conditions and the experience or expertise of the author, are based on current expectations, estimates, opinions and/or beliefs of the author. Such statements are not facts and involve known and unknown risks, uncertainties and other factors. Past events and trends do not predict or guarantee or indicate future events or results.

https://www.cnbc.com/2021/09/09/america-has-1point73-trillion-in-student-debtborrowers-from-these-states-owe-the-most.html

https://www.edly.co/?utm_source=financialsamurai&utm_medium=review&utm_campaign=edly

https://www.insidehighered.com/quicktakes/2021/09/08/federal-agency-acts-against-income-share-agreement-lender